Sustainable Energy - July Commentary

Portfolio Manager, Specialist Team

Portfolio Manager, Specialist Team

This is a marketing communication. Please refer to the prospectus, supplement and KID/KIID for the Funds before making any final investment decisions. The value of this investment can fall as well as rise as a result of market and currency fluctuations. You may not get back the amount you invested.

Past performance does not predict future returns.

Sustainable energy equities performed well in the first half of 2026. The energy shock as a result of the conflict in the Middle East has strengthened the case for the energy transition through the lenses of energy security and energy flexibility. Meanwhile, the underlying secular drivers of rising electricity demand continue to build, creating a greater need for both renewable power and efficiency solutions. After the tariff and tax credit uncertainty of 2025, policy has moved from a source of great uncertainty to relative stability. Against this backdrop, the sector has outperformed markets over the last six months, and we remain optimistic for the second half of the year. In this report, we review macro developments in the first half of 2026 and offer an outlook for the rest of 2026 and beyond.

The backdrop to the global energy transition in the first half of 2026 has been constructive as a result of the Iran shock, secular growth and policy stability.

Iran shock

The Middle East crisis triggered a material disruption to global energy markets, removing around 14 million barrels per day of oil and oil products from global supply with no easy alternative route to market. While the peace deal agreed in mid-June has allowed the gradual reopening of the Strait of Hormuz, with vessel transits recovering to pre-conflict levels (c.30/day as of late June), the pace of the recovery remains uncertain. Tankers remain dislocated globally, field restarts must be handled with extreme care, and infrastructure damage in the Gulf, notably to liquefied natural gas facilities, will take time to repair.

By the time oil flows normalize, we estimate that around 2.3bn bls of oil and oil equivalent will have been lost because of the conflict, around a quarter of global inventories. This represents the second global energy shock in just four years, strengthening the case for sustainable energy technologies as a way to improve both energy security and energy flexibility, especially in economies reliant on energy imports such as Europe.

- Energy security: reducing reliance on energy imports. This is of particular importance to the EU, which still imports nearly 60% of its energy from outside of the bloc.

- Energy flexibility: building a more diverse and adaptable energy system through distributed renewables, storage, and greater interconnectivity of energy assets.

Energy dependence (imports as % of total energy consumption)

Source: BofA Global Investment Strategy, Energy Institute Statistical Review of World Energy, June 2026

Secular growth: Demand for electricity continues to rise. Having grown at 2.8% per annum over the past decade, global electrification is expected to cause it accelerate to 3.6% per annum to 2030. According to the International Energy Agency (IEA), 2024 was the first year in three decades that global electricity demand outpaced GDP growth, and this gap is expected to persist over at least the next five years thanks to three structural drivers.

The first is regional. Developed markets are seeing the return of electricity demand growth after nearly 20 years of stagnation. In Europe, electricity demand growth was close to 0% between 2003-2023, but is forecast to average 2.3% growth annually from 2026-2030. The United States faces a similar trajectory; after averaging electricity demand growth below 1% per annum between 2016-2025, power consumption is now expected to grow at closer to 2% per annum to 2030.

The second is sectoral. New, durable sources of demand are complementing established ones. Data centres and AI are an important driver, particularly in the United States, where they are expected to account for 50% of incremental demand growth until 2030. However, at a global level they account for little more than 8% – less than the electrification of transport, which accounts for almost 1.5x the growth of data centres over the same period at around 12% of incremental demand growth. Industry and buildings are the largest contributors at 36% and 27% respectively, reflecting the electrification of industrial processes and the greater intensity of electrification within buildings (heating, cooling, internet of things, and automation).

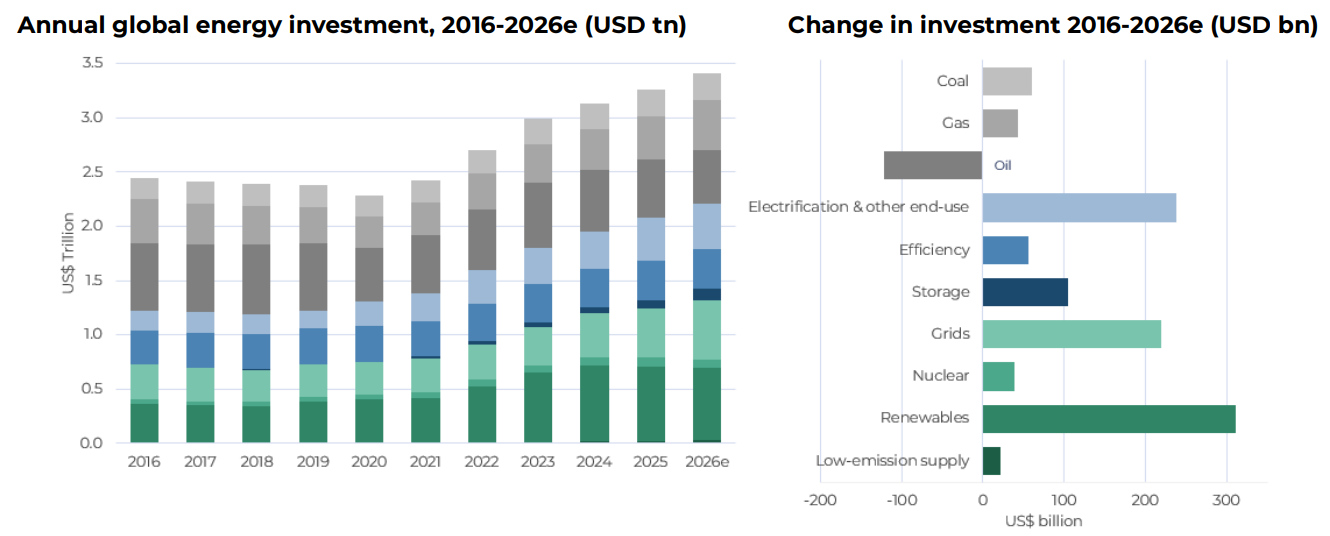

The third is transitional, with electricity winning share from hydrocarbons in the global energy mix. Electricity consumption is now projected to grow at least 2.5 times faster than overall energy demand to 2030. This is reflected in investment into sustainable energy technologies now accounting for almost two-thirds of total energy spending in 2026, totalling $2.2 trillion across clean energy generation, grids and efficiency technologies.

Source: IEA, May 2026

Policy stability

After the tariff and tax credit uncertainty of 2025, policy headwinds in the United States have eased. A year ago, sustainable energy equities faced pressure from both tariffs and the downsizing of the Inflation Reduction Act (IRA) into the One Big Beautiful Bill (OBBB). This year, the threat of structurally higher US tariffs was mitigated by a Supreme Court judgment in February which deemed them to be unlawful under the International Emergency Economic Powers Act. While there are other routes for the executive to impose replacement tariffs, these are much more cumbersome to implement (Section 232 and 301) or are more temporary in nature (Section 122).

The resolution of the OBBB has also provided the industry with much needed clarity. Although the bill is objectively less favourable to clean energy than the IRA (eliminating EV and residential solar tax credits and speeding up the phase-out of utility solar and wind tax credits) the final cuts were not as bad as expected, with support for solar and battery manufacturing even being enhanced. With policy clarity, developers have returned to the market, resulting in strong orders for clean energy equipment names such as Vestas, which reported one of its highest-ever order intakes in North America in the second quarter of 2026.

In Europe, policy remains supportive. In late April, the European Commission published AccelerateEU, its response to the energy crisis, building on the existing REPowerEU and Clean Industrial Deal frameworks. Of its five pillars, three directly support the energy transition: 'more homegrown clean energy', 'stepping up our energy system', and 'boosting investment'. The plan reaffirms existing EU ambitions, including installing around 100 GW of renewable capacity annually and increasing economy-wide electrification to 32% by 2030, up from 23% today, with more detail to come from the Electrification Action Plan due later this summer. AccelerateEU also introduces a new objective to expand installed energy storage capacity from around 55 GW to 200 GW by 2030.

In China, June saw the release of the Energy Sector’s 15th Five-Year Plan (FYP), setting out national targets including reaching 50% non-fossil electricity generation (renewables, biomass, hydro, nuclear) by 2030, compared with just over 40% today with energy security stated as the plan’s primary objective. On the demand side, electricity’s share of final consumption is targeted to rise from 30% to 35% by 2030, alongside a 30% increase in transmission and distribution spending. The new targets sit alongside China’s ongoing 'anti-involution' drive to replace years of destructive price competition with more stable industry structures, supportive for both the size and profitability of its clean energy industry.

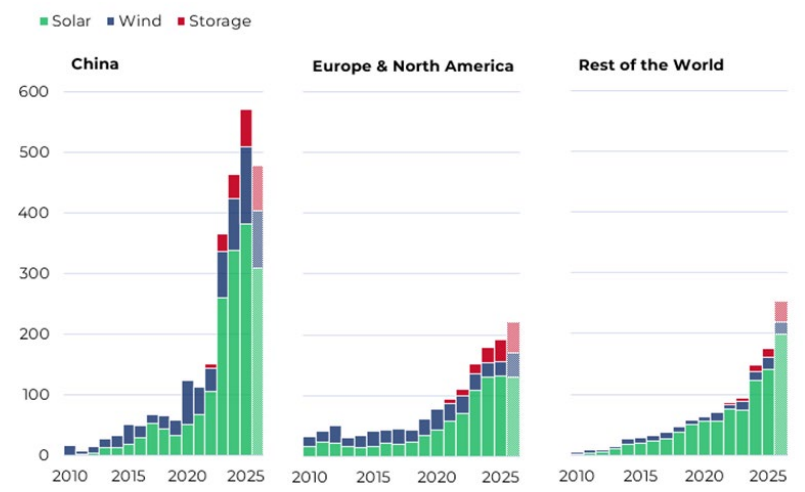

Annual renewable capacity additions by region 2000-2026E (GW)

Source: BNEF; Guinness Global Investors; June 2026

Outlook

Looking to the remainder of 2026 and beyond, we expect momentum to continue for energy transition equities, with macro and market conditions supportive of robust longer-term growth:

- Renewable power generation is expected to grow by around 1,000 TWh per annum through 2030 with solar PV representing around 60% of incremental output. This translates into clean energy production growth of 8% per year out to 2030 with renewables and nuclear expected to account for around half of global power supply by 2030.

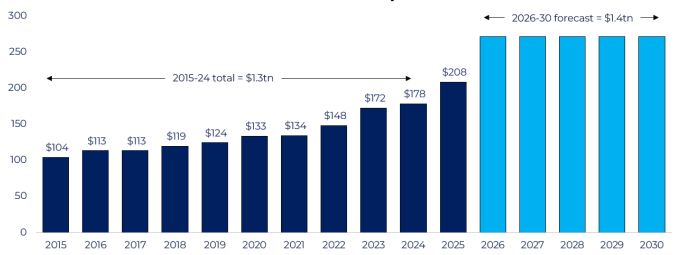

- Grid investment will increase to support this growth in renewables globally, driven by both corporates and governments alike. In the US, whilst utility capex growth is expected to revert back to its long run average of 7% per annum in 2026 after a material step up in 2025, the quantum of spending is substantially higher. Utilities are expected to spend as much in the next five years ($1.4tn) as they did in the preceding decade, with distribution and transmission now making up 50% of the budget, up from 45% a decade ago.

US Electrical Utilities Capex Forecast

Source: Power Lines, Edison Electrical Institute, April 2026

- Building efficiency and electrification spending is expected to rise 5% from around $370bn last year to over $390bn in 2026, marking a return to growth following a year of weak construction activity in 2025. Europe remains the largest market for building efficiency spending, making up 30% of global demand. Here, we continue to see encouraging signs of growth, with heat pump sales increasing by 17% year-on-year in the first quarter of 2026.

- Electric vehicle sales are expected to grow by around 11% to 23 million units, with EV penetration reaching 27% globally despite the removal of purchase tax credits in the US and scrappage schemes in China. After a material slowdown in Chinese vehicle purchasing in late 2025, early 2026 data shows signs of stabilisation with a return to growth expected in 2H 2026. Longer-term, we see global EV penetration continuing to increase, reaching 45% by 2030.

- Battery prices remain supportive to our electric vehicle forecasts, with average pack prices expected to fall 3% in 2026 to $105/kWh – just above the $100/kWh threshold at which electric vehicles become cost competitive with internal combustion engines – continuing on a journey to $70-80/kWh by 2030.

- Solar installations are expected to fall for the first time on record as the Chinese market, responsible for just under 60% of demand, transitions from feed-in-tariffs to a market-based pricing system for generators. Despite weakness in China, we continue to see growth in North America, the Middle East and in Africa with stronger module prices supported by higher raw material costs (e.g. silver) and China’s anti-involution efforts to curb excess supply. Beyond 2026, we expect solar PV’s positioning at the bottom of the cost curve to drive continued share gain in the energy mix, with BNEF forecasting solar energy to grow from 11% of global power supply in 2026 to 21% by 2032 (Economic Transition Scenario), overtaking coal as the largest source of electricity supply in the world.

- The global wind industry is on track to deliver c.154 GW of installations in 2026. Whilst headline installations are set to contract by around 10%, this is primarily driven by China, where installations are expected to fall by around a quarter this year. This follows a surge in Chinese deployments in 2025 to lock in more favourable power price guarantees under the previous regime. European wind installations are set to rise by around 60% in 2026, reaching a new record high of over 27 GW. We expect similarly strong growth in North America as developers return to the market following the passing of the OBBB.

The outlook we summarise here is broadly consistent with current government activity and observable investment plans. To be clear, however, the growth described falls well short of the energy transition activity needed to achieve a net zero / 1.5 degree scenario in 2050, as targeted by the Intergovernmental Panel on Climate Change and reiterated at COP28. In a net zero scenario, the deployment of renewable generation capacity, penetration of EVs and battery storage, use of alternative fuels and implementation of energy efficiency measures will need to accelerate markedly.

At 30 June 2026, the Guinness Sustainable Energy Fund traded on a 2026/27 price-earnings ratio of 22.0x/18.2x. On a 12-month forward view, the Fund trades at about a 5% P/E premium to the MSCI World Index, with consensus forecasts suggesting it will deliver similar earnings growth (15.3%pa vs the MSCI World at 15.1%pa). Despite offering comparable valuation and earnings growth characteristics in the near term, we continue to believe that the durability of our portfolio’s earnings growth is underappreciated, as we expect companies providing decarbonisation solutions to benefit from multi-decade growth tailwinds caused by the energy transition.

Valuation and earnings growth of the Guinness Sustainable Energy Fund

Source: Guinness Global Investors (30 June 2026)

Portfolio company NextEra Energy is a prime example of this durability, having in the first quarter reaffirmed its long-term earnings growth outlook of 8% and above annually through 2032 and 2035, underpinned by management's confidence in a "golden age of power demand" in the US. This inflection in the US power market is undoubtedly a contributing factor to the record pace of US power and utilities M&A: deal value in the first five months of 2026 alone already exceeded $200bn – surpassing the whole of 2025 ($143bn) in under half the time, itself already nearly four times the 2017–23 average. NextEra announced its own move to join the acquisition spree with a $67bn offer to acquire Dominion Energy, expanding the company's regulated utility footprint whilst bolstering its exposure to data centre-driven demand growth.

Following almost two years of de-rating, the 12-month forward P/E of the Fund has now re-rated to trade at a small premium to the MSCI World Index, reflecting improving policy clarity in the United States, the structural inflection in electricity demand, and the demonstrated improvement in sector profitability.

12-month forward P/E relative of Guinness Sustainable Energy Fund vs MSCI World Index

Source: Guinness Global Investors (30 June 2026)

Catalysts for the rest of the year include potential funding announcements related to AccelerateEU. The sector would also be a beneficiary of looser monetary policy, lower inflation and lower US Treasury yields, while any disruption to the normalization of energy flows in the Middle East and the higher fossil fuel prices that may accompany it would further improve the relative economics of renewable technologies. Further, the sector continues to benefit from the deployment of data centres and further AI capex announcements, which add to the electricity demand pool.

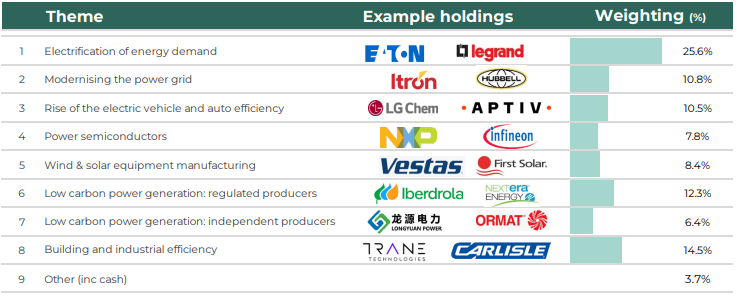

We believe that the Guinness Sustainable Energy portfolio of 30 broadly equally weighted positions, chosen from our universe of around 300 companies, provides concentrated exposure to the theme at attractive valuation levels relative to both near-term and long-term earnings growth expectations.

Key themes in the Guinness Sustainable Energy Fund

Source: Guinness Global Investors (30 June 2026)

For our full report, including analysis of fund returns in the first half of the year, click below.

The value of this investment can fall as well as rise as a result of market and currency fluctuations. You may not get back the amount you invested.

The information provided on this page is for informational purposes only. While we believe it to be reliable, it may be inaccurate or incomplete. Any opinions stated are honestly held at the time of publication, but are not guaranteed and should therefore not be relied upon. This content should not be relied upon as financial advice or a recommendation to invest in the Funds or to buy or sell individual securities, nor does it constitute an offer for sale. Full details on Ongoing Charges Figures (OCFs) for all share classes are available here.

The Guinness Sustainable Energy Funds invest in companies involved in the generation, storage, efficiency and consumption of sustainable energy sources (such as solar, wind, hydro, geothermal, biofuels and biomass). We believe that over the next twenty years the sustainable energy sector will benefit from the combined effects of strong demand growth, improving economics and both public and private support and that this will provide attractive equity investment opportunities. The Funds are actively managed and use the MSCI World Index as a comparator benchmark only.

For the avoidance of doubt, if you decide to invest, you will be buying units/shares in the Fund and will not be investing directly in the underlying assets of the Fund

Guinness Sustainable Energy Fund

Documentation

The documentation needed to make an investment, including the Prospectus, the Key Investor Information Document (KIID), Key Information Document (KID) and the Application Form, is available in English from www.guinnessgi.com or free of charge from the Manager: Waystone Management Company (IE) Limited, 2nd Floor 35 Shelbourne Road, Ballsbridge, Dublin DO4 A4E0, Ireland; or the Promoter and Investment Manager: Guinness Asset Management Ltd, 18 Smith Square, London SW1P 3HZ.

Waystone IE is a company incorporated under the laws of Ireland having its registered office at 35 Shelbourne Rd, Ballsbridge, Dublin, D04 A4E0 Ireland, which is authorised by the Central Bank of Ireland, has appointed Guinness Asset Management Ltd as Investment Manager to this fund, and as Manager has the right to terminate the arrangements made for the marketing of funds in accordance with the UCITS Directive.

Investor Rights

A summary of investor rights in English, including collective redress mechanisms, is available here: https://www.waystone.com/waystone-policies/

Residency

In countries where the Funds are not registered for sale or in any other circumstances where their distribution is not authorised or is unlawful, the Funds should not be distributed to resident Retail Clients. NOTE: THIS INVESTMENT IS NOT FOR SALE TO U.S. PERSONS.

Structure & Regulation

The Funds are sub-funds of Guinness Asset Management Funds PLC, an open-ended umbrella-type investment company, incorporated in Ireland and authorised and supervised by the Central Bank of Ireland, which operates under EU legislation. The Funds have been approved by the Financial Conduct Authority for sale in the UK. If you are in any doubt about the suitability of investing in these Funds, please consult your investment or other professional adviser.

Switzerland

This is an advertising document. The prospectus and KID for Switzerland, the articles of association, and the annual and semi-annual reports can be obtained free of charge from the representative in Switzerland, Reyl & Cie SA, Ru du Rhône 4, 1204 Geneva. The paying agent is Banque Cantonale de Genève, 17 Quai de l'Ile, 1204 Geneva.

WS Guinness Sustainable Energy Fund

Documentation

The documentation needed to make an investment, including the Prospectus, the Key Investor Information Document (KIID) and the Application Form, is available in English from www.waystone.com/our-funds/waystone-fund-services-uk-limited/ or free of charge from Waystone Management (UK) Limited, PO Box 389, Darlington DL1 9UF.

General enquiries: 0345 922 0044

E-Mail: wtas-investorservices@waystone.com

Waystone Management (UK) Limited is authorised and regulated by the Financial Conduct Authority.

Residency

In countries where the Fund is not registered for sale or in any other circumstances where its distribution is not authorised or is unlawful, the Fund should not be distributed to resident Retail Clients.

Structure & regulation

The Fund is a sub-fund of WS Guinness Investment Funds, an investment company with variable capital incorporated with limited liability and registered by the Financial Conduct Authority.

This Fund is registered for distribution to the public in the UK but not in any other jurisdiction. In other countries or in circumstances where its distribution is not authorised or is unlawful, the Fund should not be distributed to resident Retail Clients.

Guinness Sustainable Energy UCITS ETF

Documentation

The documentation needed to make an investment, including the Prospectus, the Key Investor Information Document (KIID), Key Information Document (KID) and the Application Form, is available in English from www.guinnessgi.com, www.hanetf.com or free of charge from the Administrator: J.P Morgan Administration Services (Ireland) Limited, 200 Capital Dock, 79 Sir John Rogerson’s Quay, Dublin 2 DO2 F985; or the Investment Manager: Guinness Asset Management Ltd, 18 Smith Square, London SW1P 3HZ.

Residency

In countries where the Fund is not registered for sale or in any other circumstances where its distribution is not authorised or is unlawful, the Fund should not be distributed to resident Retail Clients. NOTE: THIS INVESTMENT IS NOT FOR SALE TO U.S. PERSONS.

Structure & regulation

The Fund is a sub-fund of HANetf ICAV, an Irish collective asset management vehicle umbrella fund with segregated liability between sub-funds which is registered in Ireland by the Central Bank of and authorised under the UCITS Regulations.